Page 27 - Bullion World Volume 4 Issue 1 January 2024

P. 27

Bullion World | Volume 4 | Issue 1 | January 2024

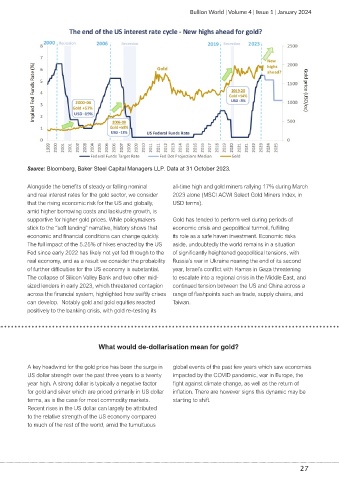

Source: Bloomberg, Baker Steel Capital Managers LLP. Data at 31 October 2023.

Alongside the benefits of steady or falling nominal all-time high and gold miners rallying 17% during March

and real interest rates for the gold sector, we consider 2023 alone (MSCI ACWI Select Gold Miners Index, in

that the rising economic risk for the US and globally, USD terms).

amid higher borrowing costs and lacklustre growth, is

supportive for higher gold prices. While policymakers Gold has tended to perform well during periods of

stick to the “soft landing” narrative, history shows that economic crisis and geopolitical turmoil, fulfilling

economic and financial conditions can change quickly. its role as a safe haven investment. Economic risks

The full impact of the 5.25% of hikes enacted by the US aside, undoubtedly the world remains in a situation

Fed since early 2022 has likely not yet fed through to the of significantly heightened geopolitical tensions, with

real economy, and as a result we consider the probability Russia’s war in Ukraine nearing the end of its second

of further difficulties for the US economy is substantial. year, Israel’s conflict with Hamas in Gaza threatening

The collapse of Silicon Valley Bank and two other mid- to escalate into a regional crisis in the Middle East, and

sized lenders in early 2023, which threatened contagion continued tension between the US and China across a

across the financial system, highlighted how swiftly crises range of flashpoints such as trade, supply chains, and

can develop. Notably gold and gold equities reacted Taiwan.

positively to the banking crisis, with gold re-testing its

What would de-dollarisation mean for gold?

A key headwind for the gold price has been the surge in global events of the past few years which saw economies

US dollar strength over the past three years to a twenty impacted by the COVID pandemic, war in Europe, the

year high. A strong dollar is typically a negative factor fight against climate change, as well as the return of

for gold and silver which are priced primarily in US dollar inflation. There are however signs this dynamic may be

terms, as is the case for most commodity markets. starting to shift.

Recent rises in the US dollar can largely be attributed

to the relative strength of the US economy compared

to much of the rest of the world, amid the tumultuous

27