-

Gold Monthly: Gold�s hot run continues

Mon April 08 2024

Gold has started the new quarter by setting record after record. Its historic rally continues amid the prospect of monetary easing by major central banks and as tensions in the Middle East and Ukraine boost its safe haven appeal

Gold hits another record high

Spot gold prices just set another record above $2,350/oz, and are now up 13% since the beginning of the year. The precious metal has had a record-breaking run since mid-February, boosted by expectations for US rate cuts, geopolitical tensions and China�s economic woes.

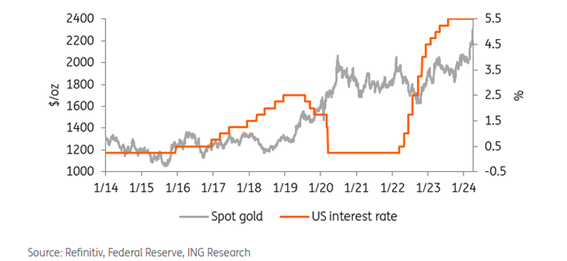

The key driver of the outlook for gold prices for the past year has been Federal Reserve policy, with rising optimism surrounding the central bank inching closer to the much-anticipated pivot fuelling the precious metal�s rally. The Fed is expected to cut this year, but has said that it needs to see more evidence of inflation easing first. The market will be closely watching US March inflation data scheduled for release later this week.

US Fed policy is a key driver for gold

Source: Refinitiv, Federal Reserve, ING Research

If the Fed continues its cautious approach to easing, gold prices risk a pullback. We expect gold prices to remain volatile in the coming months as the market reacts to macro drivers, tracking geopolitical events and Fed rate policy.

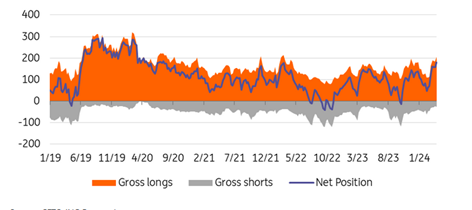

Investors turn bullish on gold

Source: CFTC, ING Research

Surging prices push gold net positions up

Investors� interest in gold finally returned, with the latest Comex data showing money managers adding fresh long positions, reflecting bullish sentiment in the gold market. Looking further ahead, we believe we will see more long positions being added given higher gold prices as US interest rates are expected to fall.

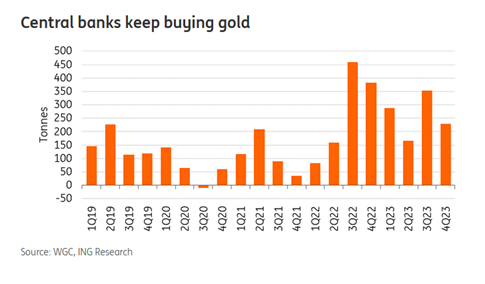

Central bank buying supports gold

Gold has also been supported by strong central bank buying as reserve diversification and geopolitical concerns have pushed them to increase their allocation towards safe assets. Central banks bought 1,037 tonnes of gold last year, just shy of the all-time high of 2022.

Central banks continued to add to their gold holdings in February (although at a slower pace than before), buying a net 19 tonnes. This marked the ninth consecutive month of growth, according to the latest data from the World Gold Council.

China�s appetite for gold has been particularly strong, with the People�s Bank of China purchasing gold for its reserves for the 17th month straight in March. China�s official reserve assets in March rose to the highest since November 2015.

Gold tends to become more attractive in times of instability, when investors pile into safe-haven assets as a hedge against the economic climate, geopolitical tensions or inflation. We believe this is likely to continue for the rest of this year.

Central banks keep buying gold

Source: WGC, ING Research

2023 gold reserves by region

Source: WGC, ING Research

However, ETF holdings in gold � which, during the Covid pandemic, were the driver behind gold�s surge to then-record highs � remain unaligned with price action. Investor holdings in gold ETFs generally rise when gold prices gain, and vice versa. Gold ETF holdings have been in decline for much of 2024, while spot gold prices are up around 13%. There is plenty of room for investors to buy the gold market, but maybe we need to wait for the Fed to actually start cutting rates before investors jump fully into the market.

Gold ETF holdings diverge from prices

Source: Refinitiv, ING Research

Gold�s Fed-fuelled rally to continue

We expect gold prices to trade higher this year as safe-haven demand continues to be supportive amid geopolitical uncertainty with the ongoing wars and the upcoming US election. We have revised our 2024 gold forecast higher, and we now expect prices to peak in the fourth quarter, averaging $2,300/oz. We expect an average of $2,206/oz in 2024 on the assumption that the Fed starts cutting rates in the second half of the year, the dollar and yields weaken, and geopolitical risks continue to support. Downside risks revolve around US monetary policy and dollar strength. The higher-for-longer narrative could see a stronger dollar for longer and weaker gold prices.

Geopolitics, Fed will support higher gold prices in 2024

Source: Refinitiv, ING Research

ING forecast

Source: ING Research

Source: https://think.ing.com/